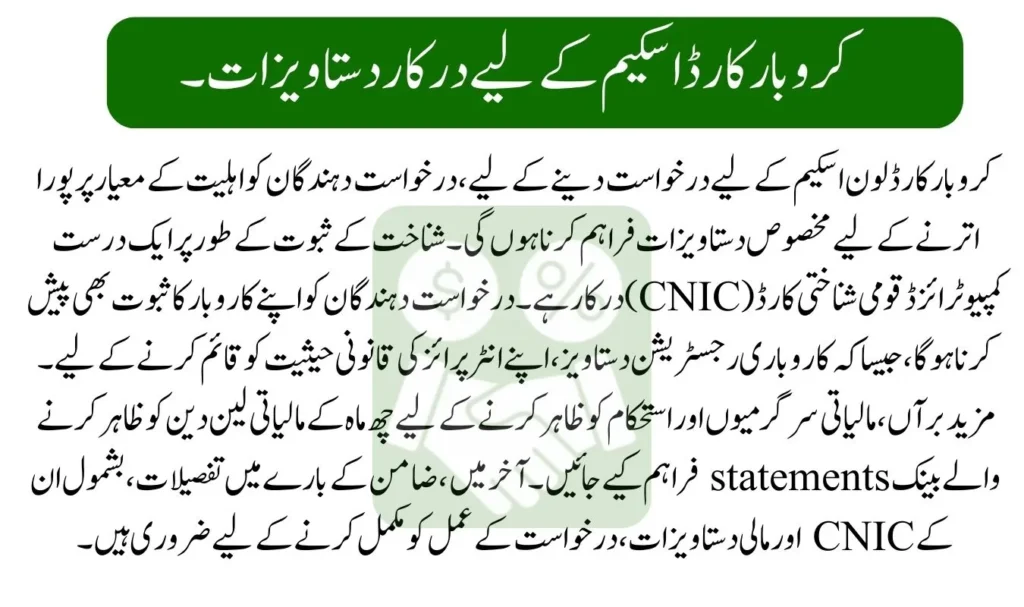

The Karobar Card Loan Scheme launched by the Punjab Government is designed to support small and medium-sized businesses by providing interest-free loans. To apply for this scheme, applicants must submit specific documents to verify their eligibility and ensure a smooth application process. This guide explains the required documents, their purpose, and how they help streamline the application procedure.

| Details | Requirements |

| Applicant’s ID | Valid CNIC |

| Proof of Business | Business registration document |

| Bank Statements | Six months of transactions |

| Guarantor Info | CNIC and financial documents |

Why Documents are Necessary for the Loan Scheme

The documents required for the Karobar Card Loan Scheme help ensure that the loan benefits are given to the right individuals and businesses. They verify the applicant’s identity, financial stability, and business legitimacy. Additionally, they help the authorities assess the ability to repay the loan within the given timeframe. Providing accurate and complete documents makes the process transparent and efficient.

CNIC – A Primary Identity Proof

Applicants must submit a valid Computerized National Identity Card (CNIC) issued by NADRA. This is the primary document for verifying the applicant’s identity and confirming their residency in Punjab. It also ensures that only eligible individuals are granted the loan.

Proof of Residence

To establish that the applicant is a resident of Punjab, they must provide proof of residence. Acceptable documents include:

- Recent utility bills (electricity, gas, or water)

- Domicile certificate

- Rent agreement (if applicable)

These documents confirm the applicant’s address and link them to the province where the scheme is implemented.

Business Registration Certificate

For small or medium enterprises, having a registered business in Punjab is a mandatory requirement. The business registration certificate or other official documentation serves as proof that the applicant owns or operates a legitimate business. This ensures that the loan is utilized for business growth and not for personal expenses.

Bank Statements

Applicants are required to submit their bank statements for the past six months. This is essential to assess the financial activity and stability of the business. It also helps the authorities determine whether the applicant can repay the loan in easy installments.

Business Plan – A Key Document

A well-drafted business plan is crucial to explain how the loan amount will be used. It should include:

- Proposed use of funds

- Business goals

- Expected growth and repayment strategy

A well-prepared business plan significantly enhances the likelihood of loan approval by showcasing the applicant’s commitment, detailed planning, and the potential for the business to succeed.

Guarantor Documents

In some cases, applicants may be required to provide a guarantor’s CNIC and financial documents. This acts as a safety net for the loan issuer. The guarantor promises to pay back the loan if the applicant cannot do so.

Photographs and Income Proof

- Photographs: Applicants must submit recent passport-sized photographs.

- Income Proof: Documents such as salary slips or revenue records help confirm the applicant’s earning capacity and ensure loan repayment capability.

Tax and Legal Compliance

Tax documents, such as the National Tax Number (NTN), are required if applicable. These show that the applicant is compliant with tax regulations, which is a vital aspect of eligibility.

Conclusion

The Karobar Card Loan Scheme has a structured document verification process to ensure transparency and fairness. By providing the required documents, applicants can facilitate quick processing and approval of their loans. This scheme is a great opportunity for small and medium-sized businesses in Punjab to grow and contribute to economic development.

You may also read: Impact of the Karobar Card Loan Scheme

FAQs

Can I apply if I don’t have a registered business in Punjab?

No, the business must be registered in Punjab to qualify for the loan scheme.

What happens if I fail to provide a guarantor?

A guarantor may not always be required, but it’s advisable to have one to strengthen your application.

How can I prepare my business plan for the loan application?

Your business plan should outline the loan’s purpose, expected growth, and repayment strategy. Consider seeking professional assistance if needed.

Is there an age limit for applicants?

The eligibility criteria will specify the age range, typically requiring applicants to be adults (18+ years).